The DBS Letters

These two signatures were purportedly taken from the same 30th July DBS letter.

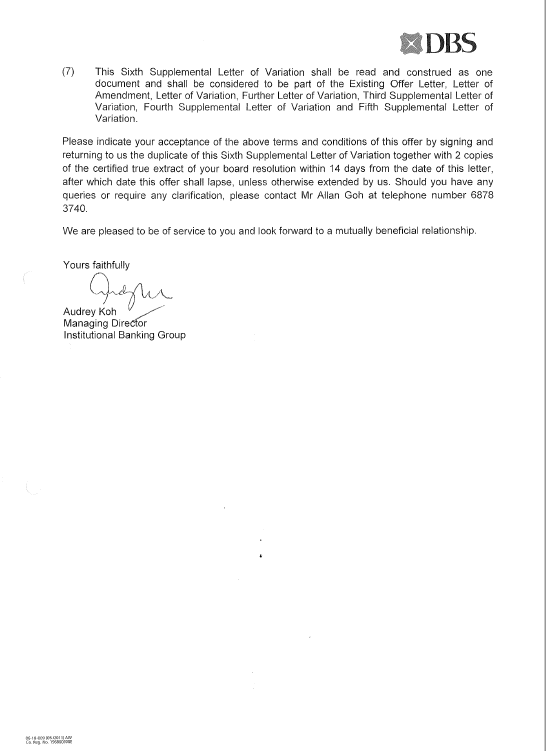

The same letter refers to itself as the Fourth Supplemental letter of Variation and the Sixth Supplemental letter of Variation. It also includes no reference number and no return address unlike earlier correspondence sent to the same client. These details were not cut off during faxing as the paper number is still visible.

But stationery number still visible - not cut off in faxing

Below is an example (highlighted) of a draft letter/template allegedly composed by Ms. Koh and sent to Strategic Marine Singapore. It displays the signature panel typically used, the font, and the inclusion of references, even in draft letters. DBS now claims that the letters above, which lack references or a return address, have not been tampered with and that they match their file copies. Are these signatures/letters authentic?

A genuine DBS Letter. The one that incredibly took almost eight-weeks to produce! OCBC sent a similar response within 48-hours.

First copy of the DBS 30 July letter received with two signatures affixed, purportedly the same document received months later with one signature missing.

The letters and the events below were just the beginning...

An influential DBS client negotiated to acquire an Australian-owned group of companies for A$1.265 million in cash, while an undisclosed scheme operated in the background. Shortly thereafter, an independent valuation conducted by BDO placed the group's true worth at between A$34 million and A$42 million. Almost immediately, DBS issued a letter threatening to foreclose on the Australian group's Singapore asset, despite being fully aware of its client's acquisition plans. That letter was subsequently used to justify a drastically reduced valuation of just A$1.17 to A$3.26 million, enabling the client to proceed with the A$1.265 million purchase.

I disrupted that transaction after receiving a sworn testimony alleging that forged signatures, implicating the client and his personal assistant, had been affixed to documents related to the acquisition.

When later contacted by an Australian lawyer, the DBS Legal, Secretariat and Compliance Department took nearly eight weeks to decline authentication of the two letters that had been used to reduce the valuation by over 90%. During that delay, the client raised funds through his SGX-listed group and completed the stripping of assets from the Australian-owned group for A$23.3 million, all while failing to disclose his potentially lucrative personal interest in the transaction when raising more than A$20 million from SGX investors.

If banking secrecy truly prevented DBS from confirming the authenticity of the letters, the institution had exposed a loophole that any scammer or white-collar criminal could exploit. When a lawyer flagged serious red flags in a transaction the bank already knew about, the responsible response should have been immediate: "We cannot authenticate this." Instead, DBS Legal replied nearly two months later, by which time the damage was done.

Subsequently, a member of the same DBS department instructed a whistleblower not to reference the letters in their submission, and not to inform DBS of that directive, even though an independent forensic examiner had already determined that the letter lacked credibility. When a former Managing Director of a Singapore GLC wrote to both past and present DBS CEOs warning of a potential whitewash, was the DBS Audit Committee asked to review what had occurred?

Authentic or Not: The Question Is Neither Hypothetical Nor Malicious